Yet another controls you to loan providers and you can researchers have quoted because perhaps elevating the cost of origination ‘s the CFPB’s Financing Originator Compensation code. The fresh new signal handles consumers by reducing financing officers’ incentives to guide borrowers towards points which have excessively high rates and charges. not, loan providers claim that by the prohibiting settlement customizations centered on a great loan’s terms and conditions otherwise conditions, the fresh code prevents all of them off lowering costs for short mortgages, especially in underserved ple, when making quick, discount, otherwise quicker-rate of interest things for the advantageous asset of users, loan providers secure reduced funds than they do off their mortgages, but as code entitles mortgage officials so you’re able to however found full settlement, people faster financing feel relatively more pricey to have lenders in order to originate. Loan providers have advised more independence in the rule would allow these to dump loan officer payment in these instances. 50 Yet not, government and experts is closely view the results from the modifications into the bank and you may borrower will set you back and you may credit availableness.

Alter into the HOEPA rule manufactured in 2013 reinforced the newest Annual percentage rate and affairs and you may costs criteria, next protecting users and limiting lenders’ capability to secure funds to your various kinds of fund

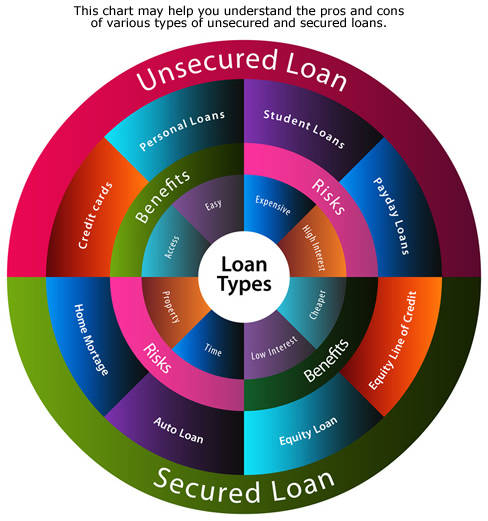

Finally, certain lenders enjoys known HOEPA as the yet another discouraging factor so you can quick mortgage lending. What the law states, enacted when you look at the 1994, handles people by the setting up constraints with the Annual percentage rate, facts and you can costs, and prepayment penalties one loan providers may charge individuals to your an extensive list of funds. Any home loan one is higher than an effective HOEPA threshold is viewed as a great high-cost mortgage, and therefore means loan providers and then make most disclosures on the debtor, have fun with given approaches to gauge the borrower’s power to pay, and steer clear of specific financing words. Likewise, the brand new 2013 change enhanced the fresh high-costs home loan thresholds, changed disclosure conditions, limited certain mortgage terms and conditions getting high-cost mortgages, and you may imposed homeownership guidance standards.

Even when eg change create all the way down lenders’ costs to originate brief mortgage loans getting underserved consumers, however they you will after that disincline loan officers of serving this segment of one’s sector and thus potentially do little to handle the short home loan scarcity

Of numerous loan providers say the fresh new 2013 transform in order to HOEPA improved the can cost you and compliance financial obligation and unsealed them to courtroom and reputational risk. However, research has shown that alter did not significantly impact the overall financing also have but have been effective in disappointing loan providers out-of originating funds one to slide over the high-cost thresholds. 51 A lot more scientific studies are needed seriously to understand how this new rule influences small mortgage loans.

A varied array of stakeholders, plus government, consumer advocates, loan providers, and you may scientists, support plan changes so you can securely remind much more brief financial credit. 52 And you may policymakers have started considering some laws and regulations to recognize people that can unknowingly limitation borrowers’ loan places Blue Ridge use of borrowing from the bank, particularly short mortgages, and also to target those products instead of limiting individual defenses.

Certain regulators have previously produced change that’ll work with the small mortgage markets by detatching the cost of mortgage origination. Such as for example, when you look at the 2022, the fresh new Federal Casing Fund Agency (FHFA) launched that to advertise sustainable and you may fair entry to houses, it could reduce be certain that fees (G-fees)-yearly charge you to Federal national mortgage association and you will Freddie Mac computer charges lenders when to shop for mortgage loans-getting financing issued to certain very first-big date, low-money, and you will or even underserved homebuyers. 53 Boffins, supporters, and the mortgage business have traditionally indicated anxiety about the outcome away from Grams-costs on the cost off mortgages having consumers, and FHFA’s transform can get keep costs down to own buyers who are really likely to explore quick mortgages. 54

Also, FHFA’s choice to expand using pc appraisals, in which a professional appraiser spends publicly offered analysis rather than a web page trip to influence an excellent property’s really worth, possess probably cut the timeframe it will take to close off home financing in addition to appraisal prices for particular loans, which often is always to slow down the price of originating short fund instead materially enhancing the risk of non-payments. 55